On Tuesday, the Government announced reforms to working age disability benefits with the stated aim of helping those who can work to do so, and supporting those who can’t. This will be done via providing more support and incentives to work, as well as making it harder to achieve eligibility for Personal Independence Payment (PIP), raising the age at which people can claim health benefits through Universal Credit (UC), and reintroducing reassessments for some people who are deemed capable to work.

The Government focusses on the increasing number of young people claiming disability benefits in their press release. However the Resolution Foundation, an independent think tank with the aim of improving the standard of living for of low to middle income families, published a report in anticipation of the upcoming announcements stating that the benefits bill is rising because Britain is getting “older and sicker”, and that cutting benefit entitlement is unlikely to lead to significant savings without causing harm and loss to disabled people.

Resolution Foundation points out that part of the reason for higher disability claims – COVID aside – is that the gap between basic and health-related Universal Credit is substantial, which incentivises those on Universal Credit to claim health-related benefits where they can.

What strikes me about this debate is that the Government discourse focuses on ensuring the young return to work, while the impact of these policy reforms will be most greatly felt by older individuals who are under the State Pension age.

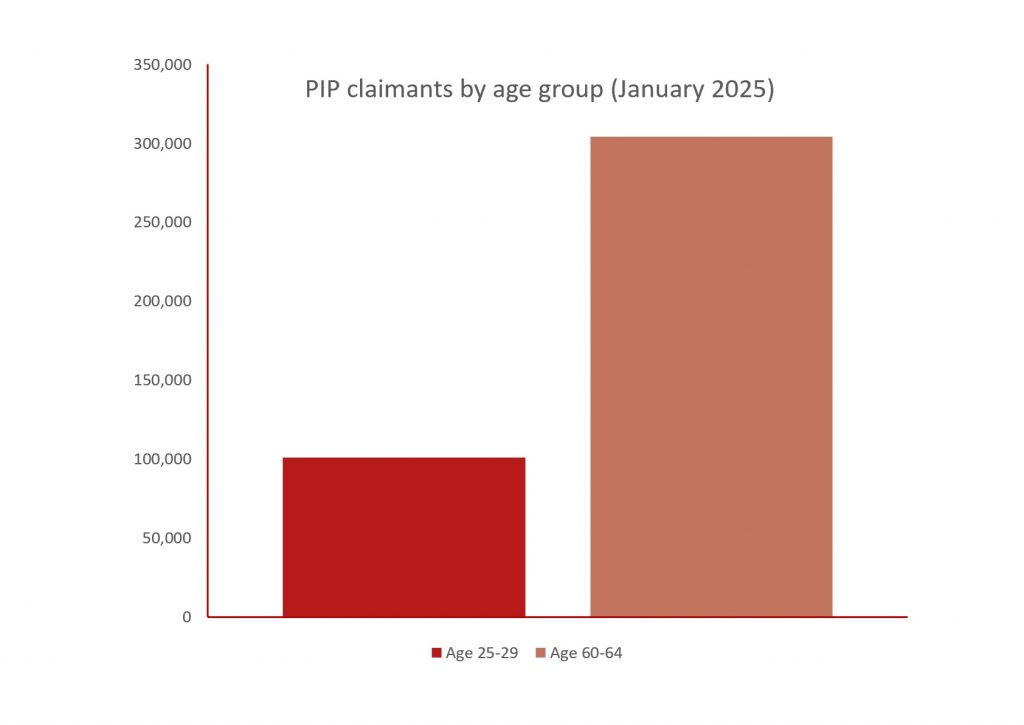

Recent data from DWP’s Stat-Xplore shows me that older people are more likely to claim PIP; In January 2025, 101,000 PIP claimants were in the 25 to 29 age bracket, compared to 304,000 claimants aged 60 to 64.

We also see a greater number of people with caring responsibilities at older ages, and more people who cannot work because of caring responsibilities or health problems.

This really matters because of the discrepancy between working life and retirement benefits. Those who leave work prior to State Pension age, due to ill health or caring responsibilities, have to wait longer for a higher benefit and may find themselves struggling on very low working life benefits. For example, a single pensioner on low income would have their income topped up to £218pw from Pension Credit, if single, with an extra amount of £82 if they have a severe disability, and/or £45.60 if they are providing care.

If you are aged over 25 and claiming Universal Credit, you’ll receive a basic rate of around £91pw, and an additional £96pw if you have a disability. So, working life benefits come in under the basic amount of Pension Credit even with a disability addition.

| Basic Weekly Amount (£) | With Disability Addition (£) | With Care Addition (£) | With Both (£) | |

| Pension Credit (Single) | £218 | £300 | £264 | £345 |

| Universal Credit (over 25) | £91 | £187 | £173 | £269 |

This is hard for those pensioners who are waiting for a higher State Pension age, and we are seeing older people dipping into their pension savings to bridge the gap. The result of these benefit changes will be higher rates of poverty both pre- and post- State Pension age, as people spend down the savings which should be funding their retirement income.

As with many current policies, I do wonder at the speed and scale of impact. I think there is a case for conducting impact assessments and introducing policies which are more nuanced and targeted, to ensure that older people don’t fall through the cracks.

Leave a Reply