Stacked disadvantage in retirement outcomes research report

“We’ve got no savings. I’m not in a position to ask my children for help. I’m just not in a position to be able to do that and probably wouldn’t anyway. My partner’s got two children. The eldest one has just got married and bought their first house, so they’re right on the edge. And the youngest travels away for six months and comes home for six months. So, you know, we’re at the mercy of the government.” White man, aged 60-64, disability, low opportunity area

Research by Daniela Silcock Pensions Research and Ignition House, supported by Standard Life Centre for the Future of Retirement, Pensions UK, Nest, the Centre for Ageing Better and Age UK was published on 23rd April 2026

The research examines how disadvantage builds across the life course and shapes retirement outcomes. It looks at how ethnicity, gender, disability and socio economic background affect people’s experiences of work, income, caring and health, and how this affects pension saving.

.

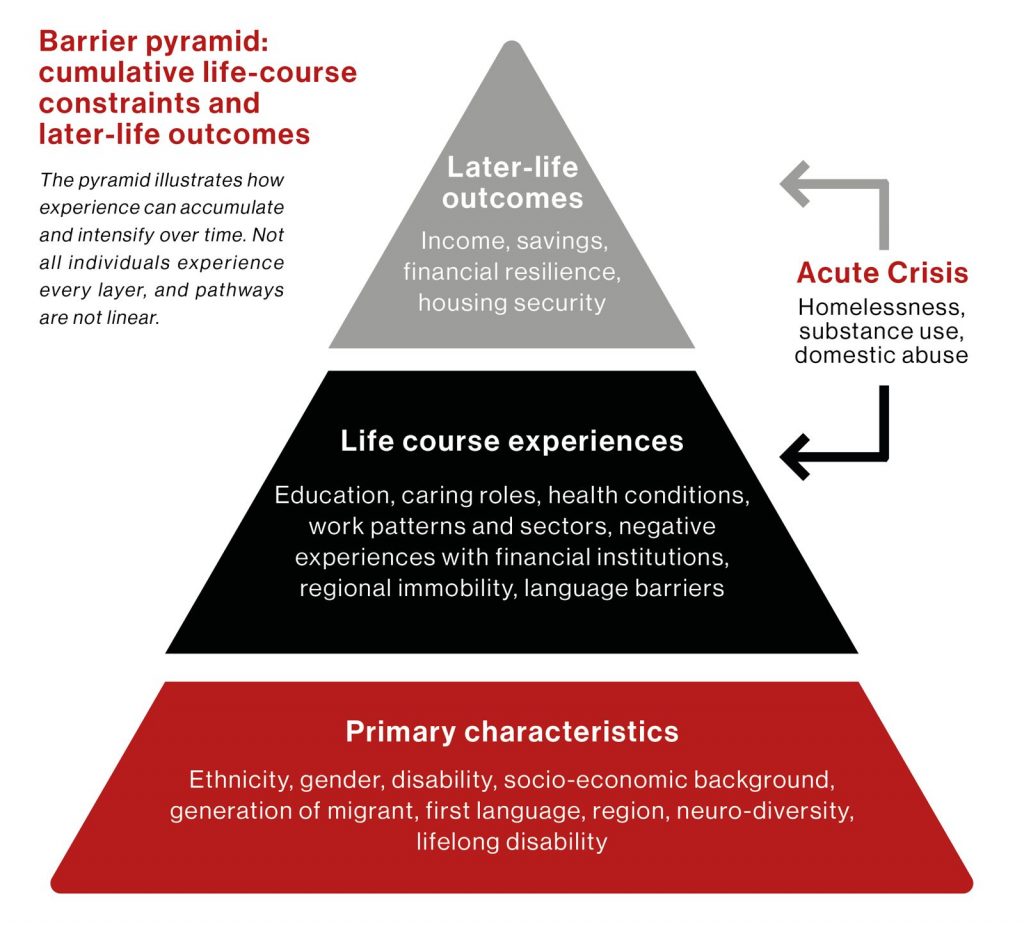

Understanding overlapping disadvantage in retirement

Current pension and related systems are designed around stable employment, steady earnings and the capacity to engage.

Primary characteristics shape lifecourse experiences

Ethnicity, gender, disability, socio-economic background and region shape how people are treated by labour markets, institutions and policy systems. These interactions affect exposure to low pay, insecure work, unpaid caring, ill health and difficulty navigating services.

Lifecourse experiences can overlap and reinforce

Lifecourse pressures overlap. Low pay limits saving and can leave little room for adapting to shocks. Insecure work makes earnings volatile and pension saving stop and start. Caring and ill health reduce hours, increase time out of work and slow progression. Discrimination and place constraints reduce access to stable and higher paid work.

Retirement outcomes reflect these patterns

Where disruption is repeated and recovery is limited, people are more likely to reach later life with lower pension saving, weaker non-pension savings, less stable housing and lower financial resilience.

The figure below above uses a set of illustrative profiles to show how stacked disadvantage can build across working life. These profiles are simplified combinations of characteristics that are repeatedly linked in the evidence base to barriers and challenges that matter for pensions and later life security.

Red means poorer outcomes are more likely, supported distinct pathways through lifecourse experiences, or by more than one source supporting the same pathway.

Amber means outcomes are mixed, evidence is less consistent, or the link rests on a single pathway, including cases where the pathway is plausible but evidence is thin.

Green means a mitigating factor is more likely to be present that could reduce risk in practice. Green does not mean good outcomes overall.

Blank cells mean no direct link was found in the reviewed evidence for that specific profile and outcome. A blank cell does not mean no link exists. It means it was not evidenced in the sources included in the review.

Related work

This research sits within a wider programme of work on how people build financial security over time, and how systems respond to different working lives.

The women’s financial future initiative

This initiative focuses on how women navigate decisions that shape long term income. It provides information via workplaces on how work, caring, relationships and financial arrangements affect pensions and retirement.

Blogs and earlier work

Related articles and previous research explore how pension systems operate in practice, including gaps in coverage, differences in outcomes between groups, and how policy design affects saving. These pieces expand on themes in this report and provide additional context.